Fitch Ratings raises short-term oil and gas

Fitch Ratings has raised its 2021 and 2022 oil price assumptions for Brent and West Texas Intermediate (WTI) benchmarks to reflect a stronger-than-expected demand recovery and supportive OPEC+ output policies. The 2021 gas price assumptions have also been increased reflecting higher demand due to the cold northern hemisphere winter and an economic rebound in Asia.

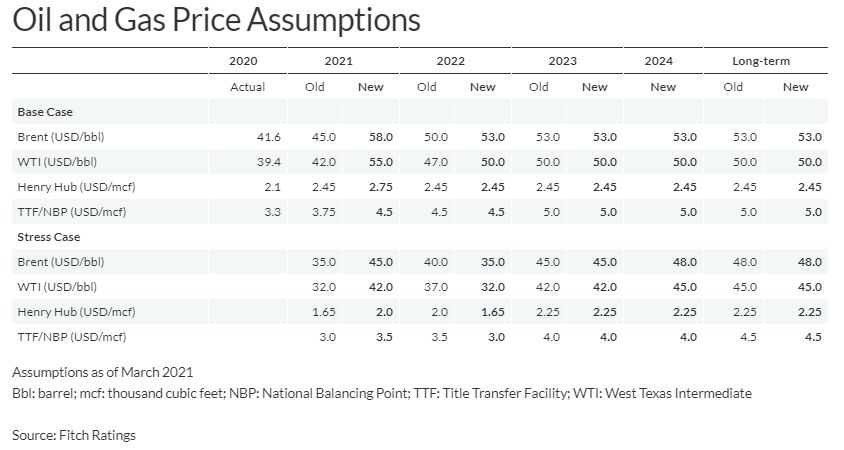

We have significantly increased our 2021 price assumptions to USD58 a barrel (bbl) from USD45/bbl for Brent and to USD55/bbl from USD42/bbl for WTI. This reflects stronger-than-expected oil demand and an economic recovery in 2H20, the fairly small impact of the latest lockdowns and other mobility restrictions, and OPEC+’s supply management, which includes Saudi Arabia’s voluntary cuts of a million barrels a day. We consider such supply management policies as being prudent. Furthermore, oil prices will continue to benefit in the short term from positive sentiment due to successful vaccination roll-outs and the upcoming USD1.9 trillion stimulus package in the US.

However, Fitch assumes prices will moderate in 2H21 and into 2022 (the market is in backwardation with near-dated prices higher than later-dated ones). We therefore only raised our 2022 assumptions by USD3/bbl to USD53/bbl and USD50/bbl for Brent and WTI, respectively. We expect OPEC+ to continue actively managing supply, at least in the medium term, and that excess oil inventories will normalise quickly. We kept longer-dated prices unchanged and these continue to incorporate the expected marginal cost of supply, as well as energy transition risks.

OPEC+ production cuts were the main driving force that helped the market rebalance fairly quickly in 2H20. On March 4, OPEC+ rolled over existing production quotas until April (Kazakhstan and Russia were allowed marginal production increases) and Saudi Arabia committed to keeping its voluntary cuts. This should accelerate inventory normalisation and support prices, at least in April. Once inventories have been normalised, we expect OPEC+ to adjust its production in line with demand to avoid significant deficits or surpluses, which could result in prices moving into the USD50/bbl-USD60/bbl range.

IEA expects demand to improve further in 2H21 as vaccination is rolled out and mobility restrictions are gradually eased. Despite the oil price recovery, US shale production is unlikely to grow at the rates seen before the pandemic due to producers’ increased focus on free cashflow generation, debt reduction and shareholder distributions, and consolidation in the sector. However, there could be a positive US supply response to the high prices in the near term.

While we expect OPEC+ to continue managing supply over the next one or two years, views on how to do so may diverge. Russia has been pushing for production increases and was effectively allocated a marginally higher quota in early 2021. In the long term, agreeing on similar deals may be more challenging. Iraq, Kuwait, Russia and the UAE are planning long-term production increases, while many producers’ output, including Saudi Arabia and the UAE, was already well below their capacity before the pandemic. Future OPEC+ discussions could be complicated by the energy transition and some countries’ desire to increase production volumes to monetise their oil reserves.

Our increased gas price assumption for 2021 reflects cold weather in the northern hemisphere in early 2021, outages at numerous LNG plants and logistical issues experienced by LNG carriers, while demand in many Asian countries has increased due to their economic rebound. European gas storage is only 34per cent full, down from 60per cent in early March 2020, supporting higher 2021 prices. We kept our prices for the rest of the period unchanged.

Source: Fitch Ratings

{kind=link}

Leave a Reply